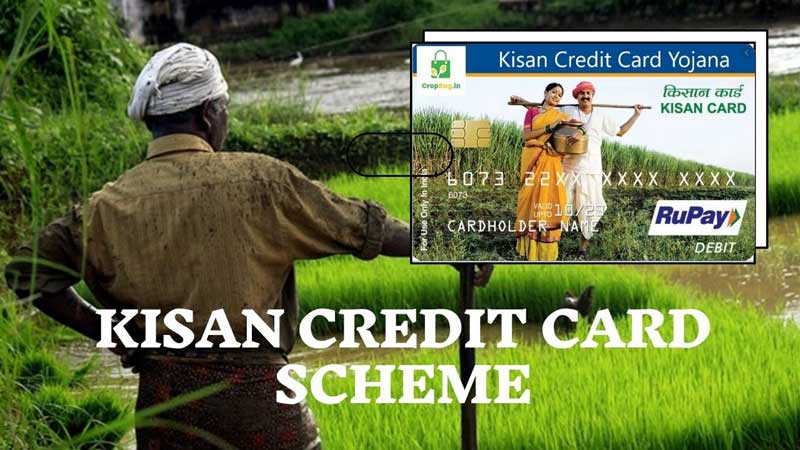

Empowering farmers and alleviating their financial burden due to rising costs of farming and unforeseen events, the Government of India introduced the Kisan Credit Card Scheme in August 1998. These cards are available through many banks, such as HDFC Bank, as well as the State Bank of India. Under the mentorship of R.V. Gupta, and the Agriculture National Bank, a committee was created to establish a credit card for farmers specifically, ensuring term loans at very low levels of interest. In the event some farmers cannot pay back loans, these may even be waived, as this is a more formal government-enforced borrowing scheme.

Unforeseen Events

Close to 70% of the Indian population depends on agriculture for their livelihood. India is a country that is known as a farming nation, with farmers playing a very important role in its economy. Nonetheless, there are unforeseen calamities, such as drought and floods that farmers may have to face, and crop yields are destroyed at such times, leaving the poor farmers penniless. Before the advent of the Kisan Credit Card Scheme, the farmer, already poverty-stricken to some degree, had to depend on local moneylenders for financial support. This informal way of lending money brought a lot of stress on the farmer, as it incurred high rates of interest when it came to paying back the loan, as well as stringent collection practices by moneylenders. In the event that there was no crop yield, the farmer would be left with the anxiety of paying back a hefty loan without any recourse to funds.

What the Credit Card Covers?

The aim of this credit card is to meet the entire needs of the agricultural sector, as well as fisheries and animal husbandry. Institutions that are participants are regional rural banks, commercial banks, and cooperative state banks. Short-term credit limits are available for crops. Term loans can also be opted for. Credit cardholders are additionally covered under insurance (personal accident) as well as disability. The card offers credit as cash credit and term credit (covering activities like land development, pump sets, irrigation, etc.).

Farmers in Mind

In the midst of protests by farmers against the government’s new farming laws, the Ministry of Finance has extended farmer strength. Announcing that the government’s goal was to ramp up agricultural growth in the country, it has introduced the Atma Nirbhar Bharat scheme. A special saturation drive to boost the rural economy, the Finance Minister, Nirmala Sitharam, stated than INR 20.97 lakh crore would be pumped into the Kisan Credit Card plan. For 2.55 crore farmers under the credit card scheme, this would mean a credit boost of INR 2 lakh crore. Mainly to tide over farmers’ troubles experienced as a fallout of the Coronavirus pandemic, this stimulus package will give farmers more in loan amounts at concessional rates.

Eligibility and Application

The interest payable on loans through the credit card is around 4%, but according to the State Bank of India, this may be waived (by 3%) when a farmer makes prompt loan repayments. Applicants should be able to show a credit of production of INR 5,000 to be eligible, plus have proof of identity and address proof (Aadhaar and PAN Cards are a must). Proof of land ownership is also required. The age eligibility is between 18 years to 75 years. In case the applicant is 60 years and over, a co-applicant (and legal heir) will be necessary. You need to hand in photographs as well to get the Kisan Credit Card online. Apply by visiting the bank’s website first. You will have to download the form and print it, then fill it, and submit the application with your requisite documents at the nearest branch of the bank chosen. The loan officer will review documents, and grant the loan.

Getting Loans

The Kisan Credit Card gives farmers a loan coverage of up to INR 3 lakh. While this is a significant amount, it may not be enough to cover the cost of all farming needs, such as buying more equipment. It’s a good idea to get the Bajaj Finserv RBL Bank SuperCard to meet any additional expenses. This card has multiple uses, and acts as an ATM card, giving you no-cost withdrawals for up to 90 days. It also serves the purpose of a loan card and an EMI card, with nominal interest rates of 1.16%.